Keniel Aeon Thomas was a happy man. He lived on the beautiful island of Jamaica basking in the sun and happily running a small home business hat was doing very well. He had no office rent to pay and, using only his telephone and email, Keniel’s business was going so well that he made a profit of at least $300,000 in a relatively short amount of time.

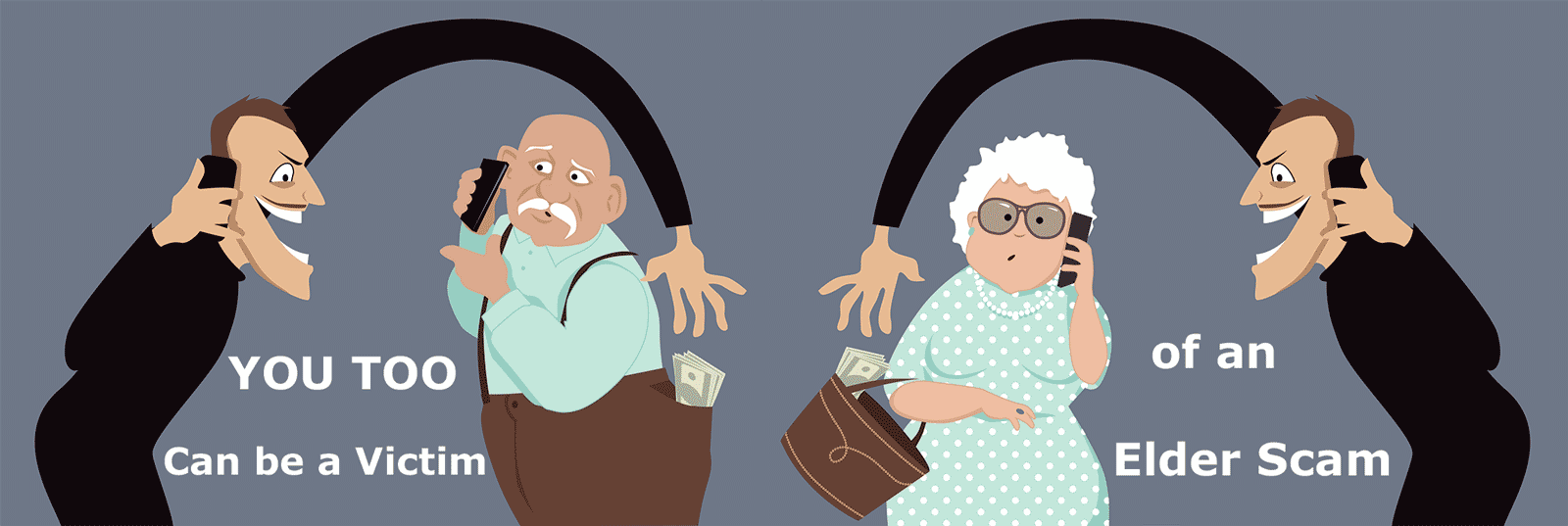

Keniel Aeon Thomas was a scam artist. He had scammed more than 30 victims. Something that is fairly common on the beautiful island of Jamaica. They target elderly people who come from a generation that instinctually trust others and want to help anyone in need and, more often than not, get away with their scams because these crimes are very difficult to prosecute due to the need for extradition

But, one morning, in 2014, Eniel Thomas called the wrong man. On the other end of his line was… a federal district and appellate court judge in the 1970s, then was appointed by Pres. Jimmy Carter to be director of the FBI and, in 1987, head of the CIA—in fact, the only person to ever hold both of those job. In addition, this man, Judge William Webster, currently chairs the Homeland Security Advisory Council.

Keniel Thomas told Judge Weber that he had just won $72 million and a new Mercedes Benz. He explained that the judge would need to send $50,000 to cover taxes and fees before the winnings would be released to him.

“You’re a great man…. you was a judge, you was an attorney, you was a basketball player, you are in the U.S. Navy, Homeland Security, I know everything about you. I even seen your photograph, and I seen your precious wife” Thomas told the judge. What Keniel Thomas did not know was that the next call was being monitored by the FBI…. Judge Webster told the man that “I am as anxious as you are to get the money” but, that it would take a while for him to collect that much money.

Thomas told him that he could send it in various payments, with a first payment of $20,000. Then he lowered the number

Thomas called numerous times, identity himself as David Morgan, a manager with Megamillion. The judge asked him to stop calling, but Thomas continued and then began sending email (more than 20 emails). Judge Webster noticed email address identified him as keniel.thomas@outlook.com not David Morgan.

One day Judge Weber’s wife Lynda answered the phone and the calls became threatening. She was told that she needed to pay $6,000 “or else”. Thomas told her that he knew that one had been at home with her the previous night. He further threatened to find her at “her white brick house” and “put a bullet straight through her head”. He said it would be “so easy that we go set your house ablaze…you can be taken care of easy” He also bragged that the FBI would never find him, and she needed to pay or she and her husband would be killed

Finally, in 2017, Keniel Thomas took a trip to New York City and the FBI grabbed him as he exited his flight from Jamaica. He pled guilty and, just a few weeks ago, went on trial.

Under normal circumstances the prison term for this sort of crime is 33 to 41 months. However, US District Judge Beryl Howell added 2 ½ years for a total of six years saying the scam qualified as organized criminal activity and the scammer presented a threat to the family members of the victim.

In court Thomas addressed the Websters saying “I really didn’t mean to hurt you guys and… we (referring to Jamaicans) love you guys, we love tourists”

His lawyer said he was disappointed by the 30 months added to Thomas’ sentence and said he was considering an appeal

From the bench, Judge Howell Addressed Judge and Mrs. Webster, saying “You continue your public service it is a real honor to have you in my court”

Jamaican based scamming has become big business in the last years. They frequently target older more vulnerable citizens and, in many cases, completely destroy their lives. Scammers pass around cell phone numbers, which is why the Webster’s continued to receive calls even after the arrest

Running scams on numerous victims these criminals launder the money by having one victim send money to a second victim before it is sent to Jamaica. A man in California told the FBI that he received certified checks in exchange for sending $85,000 for the “taxes and fees”. Not surprisingly, the certified checks all bounce.

A 75-year-old woman, receiving one of these call for man in the 876-area code (Jamaica) and having been previously warned about this sort of scam, told the man she wasn’t interested. But, before she could hang up, he began threatening her, telling her he knew where she lived and that he would put a bullet in her head.

Frightened, she told him she didn’t have any money and again hung up. He called back saying he knew she lived alone, and she would be killed. Finally, she called her cell phone company to have the number blocked and then called her local sheriff’s department.

In yet another case, an 82-year-old woman from Californian said that the man who called her identified himself as “Obama” on the phone. She sent him $600,000 in one year. A California man paid 87,000. An 85-year-old man lost his home and lifesaving. A woman in North Dakota lost more than $300,000. A man in Knoxville Tennessee committed suicide after sending thousands to a Jamaican group according to a report on CNN. Another woman received an email saying if she didn’t pay $3,000 by a certain time, members of her family would be murdered. The email stated… “we know who you are, we know where you live, we’ve been tracking you, we know your schedule, we know where you spend your time.

A California woman received a phone call one morning while she was driving to work. The man on the phone said they had abducted her mother and they were going to kill her if she did not pay. She could hear her mother’s voice in the background on the other end of the phone which made her believe that this was true. She was told to go to a nearby grocery store and put the money into a money pack card. She was then to give the man the card numbers over the phone and then destroy the card. He said they would release her mother after they got the money and received email pictures of the destroyed money card.

Somehow this call got cut off at which point the woman called her mother and the mother answered the phone. It turned out the scammer had also called the woman’s mother frightening her with a story of having kidnapped her daughter in order to obtain her frightened voice for the daughter to hear.

He did not call back.

She said she never answered phone call she did not recognize, didn’t answer block numbers, and often let people leave voicemails before she picked up. However, this call appeared to be from her mother. She said, “If it could happen to me, it can happen to anyone”.

Law enforcement says that when people get calls like this they should immediately hang up and call law enforcement. The FBI recommends that, if you get an email like this, you should not respond. Your response shows the scammer that your account is active and that will attract further contact from scammers.

Frank Abagnale, the con artist who inspired Leonardo DiCaprio’s movie Catch Me if You Can, says that things have gotten “4000 times easier” for scammers today than when he committed his crime. He, along with all law enforcement, says that we give out far too much of our personal information especially on the Internet

Mrs. Webster said that the FBI is doing wonderful work with this sort of crime and that she and her husband had chosen to speak publicly as a way to draw attention to frauds targeting older people.

The California woman, targeted with a fake kidnaping scam, was correct when she said, “If it can happen to me it can happen to anyone” We must educate ourselves about scams and financial elder abuse. These crimes will only come to an end when we are an informed, alert, and cautious citizenry.

As we have just begun, we have not yet received any letters. I certainly hope that you will write to us: tell us about your experience with Financial Elder Abuse or Involuntary Guardianship. We will also be looking for people to interview for our monthly video and lovely photographs for our cover.

As we have just begun, we have not yet received any letters. I certainly hope that you will write to us: tell us about your experience with Financial Elder Abuse or Involuntary Guardianship. We will also be looking for people to interview for our monthly video and lovely photographs for our cover.